CHIP CLIFF

03/15/26 Prospero.ai Investing - 301st Edition (Weekend)

One of the most brutal lessons hitting traders right now in this choppy 2026 market is how fast a single overlooked macro thread can unravel an entire sector narrative. Everyone’s been riding the AI supercycle wave, sky-high valuations, endless capex talk, semis acting like they print money. But the real edge comes from spotting where the assumptions break.

And right now, the break is staring us straight in the face from Taiwan.

TSMC makes about 90% of the world’s most advanced chips. Those fabs are absolute beasts — running 24/7 with zero tolerance for hiccups. Extreme ultraviolet machines, plasma etching, chemical baths… every step demands rock-solid power, stable temperature, perfect gas flows. A voltage dip that lasts seconds can trash wafers worth tens of millions. No graceful pause button. No quick reboot.Here’s the punch: those fabs already chew through nearly 9-10% of Taiwan’s entire electricity supply, and that number keeps climbing as AI demand ramps. Taiwan generates close to half its power from natural gas, almost all of it imported as LNG. Oil has big strategic reserves. LNG? Legally required buffer sits at just 11 days. A chunk of those cargoes routes straight through the Strait of Hormuz or comes from Qatar, both now squarely in the crosshairs of the Middle East mess.If flows tighten and that thin buffer starts burning faster than expected, the island can’t just flip a switch to coal and call it a day. Curtailments or even precautionary rationing hit the fabs hard. Work-in-progress wafers get ruined mid-cycle. Restarting isn’t flipping the lights back on, it means days of recalibration, weeks of requalification, and often months before yields and output claw back to full speed.That’s not a minor delay. That’s a sudden, persistent hole punched in global supply for the exact chips powering AI GPUs, phones, cars, and defense systems, right when the story assumes unlimited, uninterrupted growth.

This is why semiconductor shorts are looking more attractive by the day on Fintwit. Valuations baked in smooth sailing and cheap energy. Instead, the same regional chaos driving oil higher is quietly stress-testing the power lifeline for the entire advanced-chip ecosystem. Higher electricity costs are already nibbling at margins. Any credible whiff of rationing or LNG alerts could send the whole complex repricing fast.We’re talking about it today because this isn’t some exotic tail risk anymore, it’s a live macro threat sitting in plain sight while the market digests energy shocks and softening labor data.Let’s break down exactly how this 24/7 energy vulnerability plays out if the squeeze intensifies, and what it means for positioning in a bear market that refuses to give easy bounces.

Key takeaways should be clear from this:

Taiwan’s 11-day LNG clock is the hidden macro fuse: heavy reliance on Hormuz/Qatar-linked imports leaves the power grid one sustained disruption away from real pressure.

Fabs demand perfect 24/7 power, any curtailment doesn’t just pause production; it destroys expensive WIP and forces a slow, painful multi-month recovery to stable yields and output.

Broader ripple: hits related inputs and amplifies inflation/margin pain across tech, reinforcing defensive rotation.

Trading edge: capital preservation first, sell strength in cyclicals, keep leverage light, and treat any fresh Taiwan power or LNG headlines as high-conviction volatility catalysts.

A WORD FROM OUR CEO

We had a good week and are now 37% above the market on an annualized basis, with a 54% win rate against SPY benchmarks.

Our short intro + learning videos get you up to speed on how best use our letters and app to increase your wins.

Only one stream this week Wednesday the 18th at 3 PM.

Track all of your investments in real time with our app. Prospero’s proprietary AI tech updates key options signals like Net Options Sentiment, Upside and Downside every 3 minutes.

CHIP CLIFF

Market/Macro Update w/ Cap/ Value Analysis

QQQ and SPY Net Options Sentiment

Sector Analysis

How we view the Sector performance and momentum

Portfolio Strategy

Putting it all together to make a portfolio that first controls for risks but also has upside

Longs

Adds —> Keeps —> Drops

Shorts

Adds —> Keeps —> Drops

Portfolio Summary

CAP / VALUE ANALYSIS

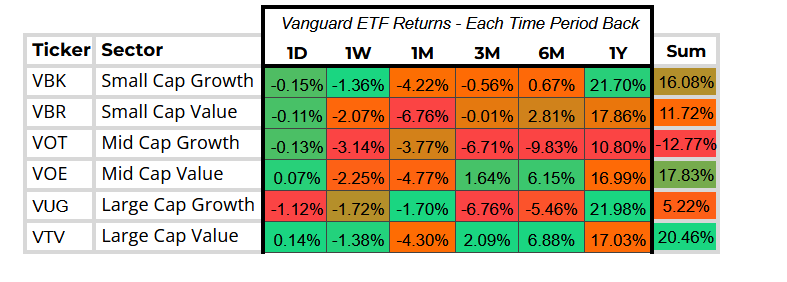

Now it was Growth’s turn this week to have a heavy contraction relative to their Value peers. Mid Caps are really feeling it regardless, they’re in a weird spot where multiples aren’t low enough and they’re more prone to geopolitical shocks than their Large Cap peers. Might not be bad to pivot back to Value right now or at least not be overexposed to Growth.

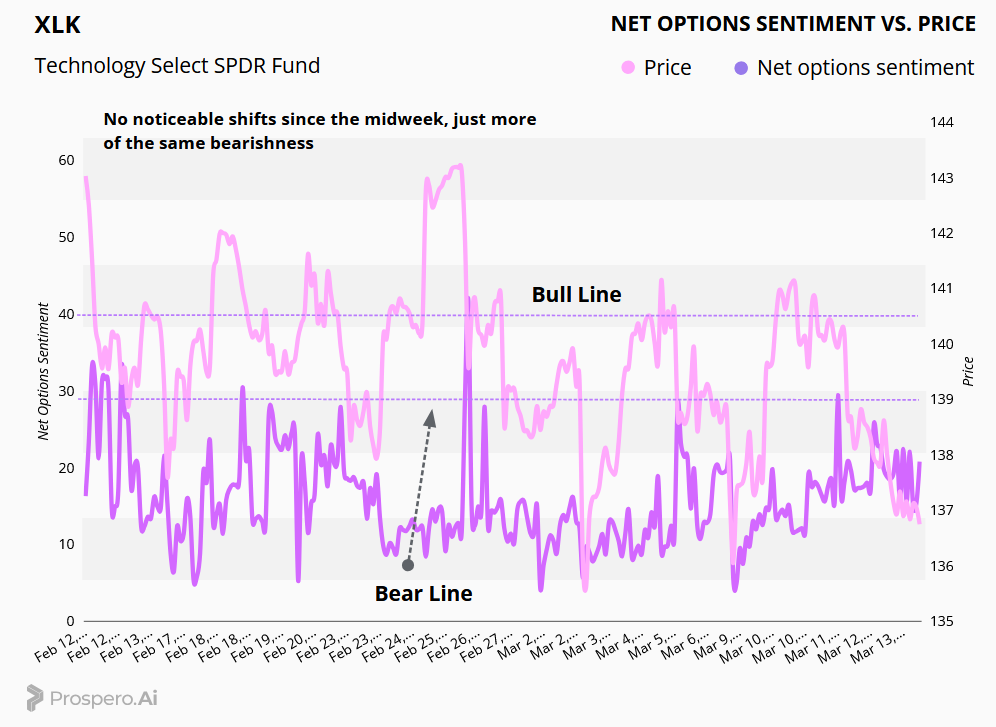

Just a Tech bear market out there, but instead of any reversion the the mean we just see stagnation in performance so far, although that could change in the medium term as multiples look a lot more attractive now than they did 6 months ago.

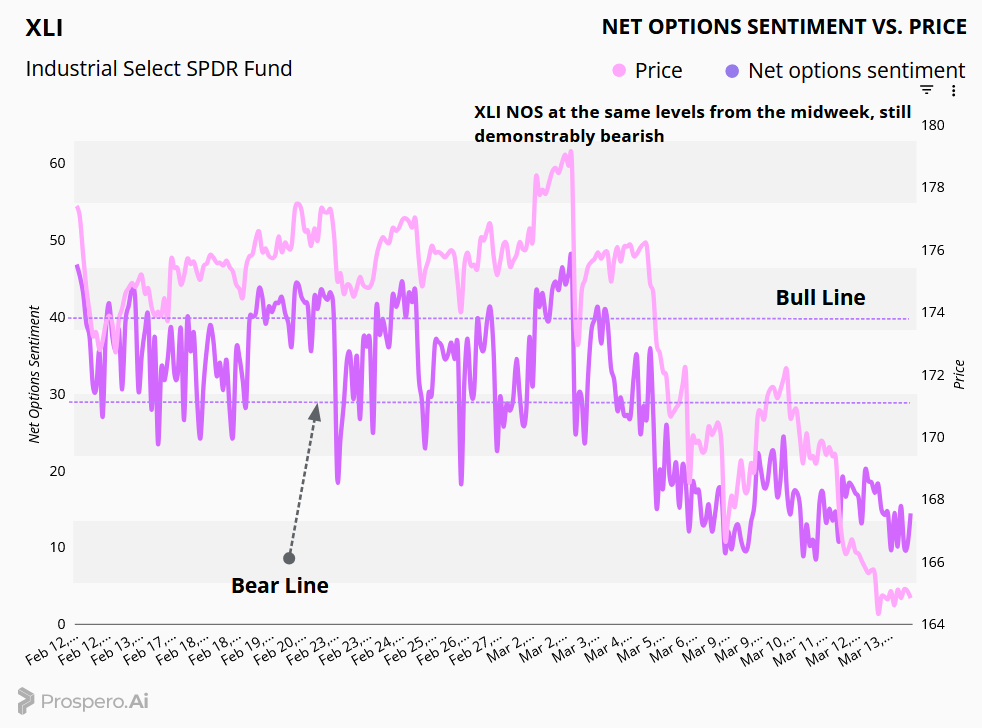

XLI NOS still bearish as it was at the start of the week and that doesn’t look like it’s changing after the poor GDP report. Not a lot of macro catalysts here to think of.

SECTOR ANALYSIS

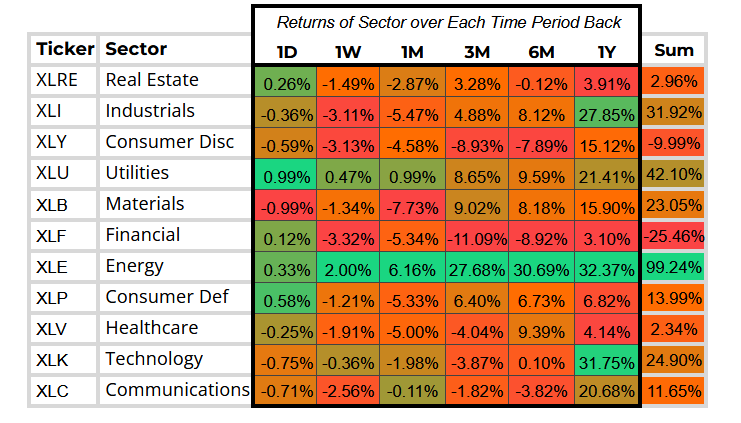

A great time to be a trader if you’re on the short side, not so much on the long side unless you were positioned into Energy or any commodities. Outside of stating the obvious, Utilities present the most compelling opportunity here honestly much more recession proof than anything. Financials remain a consensus short and should definitely be one pillar of your short exposure, and at least on a shorter time frame Consumer Discretionary and Industrials as well but would watch out for crowded trades.

PORTFOLIO STRATEGY

Heading into another bearish week in terms of sentiment overall, we’re reducing our overall exposure here, playing it safe with just our high conviction picks as the market sorts itself out. 3 Longs, 3 Shorts

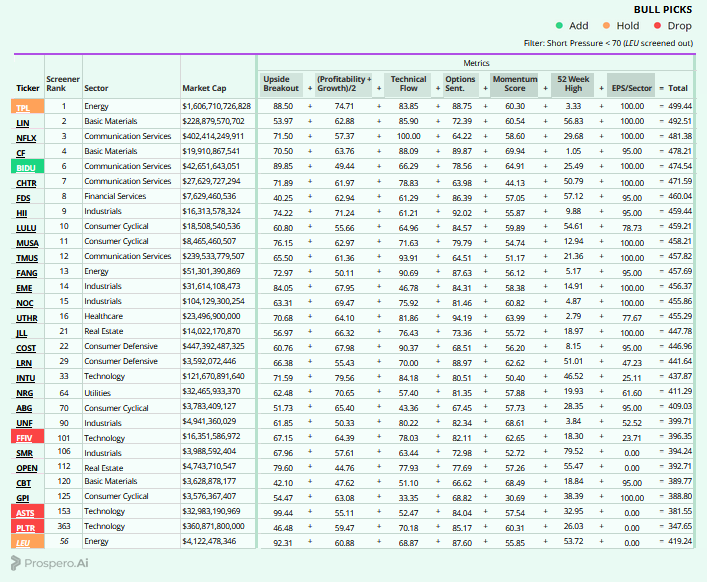

Long / Bull Moves – BIDU add / TPL and LEU holds / FFIV, ASTS and PLTR drops

Adds

BIDU looked like a well rounded pick and the best way to get some diversification away from the US market.

Holds

TPL was kept for Energy exposure and the fact that it placed at the top of our screener. LEU was kept as well for Energy exposure with good Upside Breakout and Net Options.

Drops

FFIV, ASTS and PLTR were dropped as they performed poorly in our screener this week.

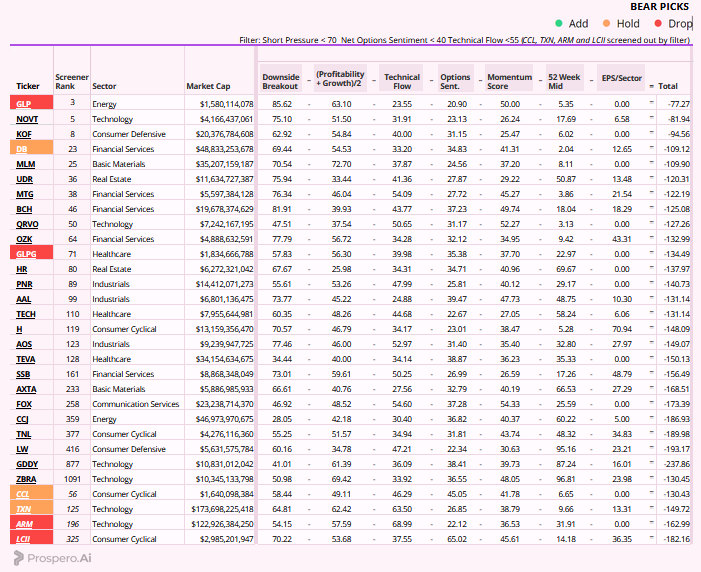

Short / Bear Moves – DB, CCL and TXN holds / GLP, GLPG, ARM and LCII drops

Holds

DB was kept for that private credit bear exposure. CCL was kept for Consumer Cyclical exposure. TXN was kept as a Large Cap Tech short with poor Net Options.

Drops

GLP was dropped as we wanted to shrink our Energy short exposure. GLPG wasn’t attractive enough this week for us. ARM and LCII were both dropped as they performed poorly in our screener.

Portfolio Summary

Long / Bull Moves – BIDU add / TPL and LEU holds / FFIV, ASTS and PLTR drops

Short / Bear Moves – DB, CCL and TXN holds / GLP, GLPG, ARM and LCII drops

3 Longs: BIDU, TPL and LEU

3 Shorts: DB, CCL, TXM

Paid Investing Letter Bonus with Momentum Score