WARSH YOUR STEP?

06/07/26 Prospero.ai Investing - 325th Edition (Weekend)

Today we are getting a rare a rare letter from George Kailas (me) writing the intro myself. I’ll be gone for 3 weeks to Paris, Greece and Ghana! Matt is out plus I think this is an interesting week so awaaaaayyy we gooooo…

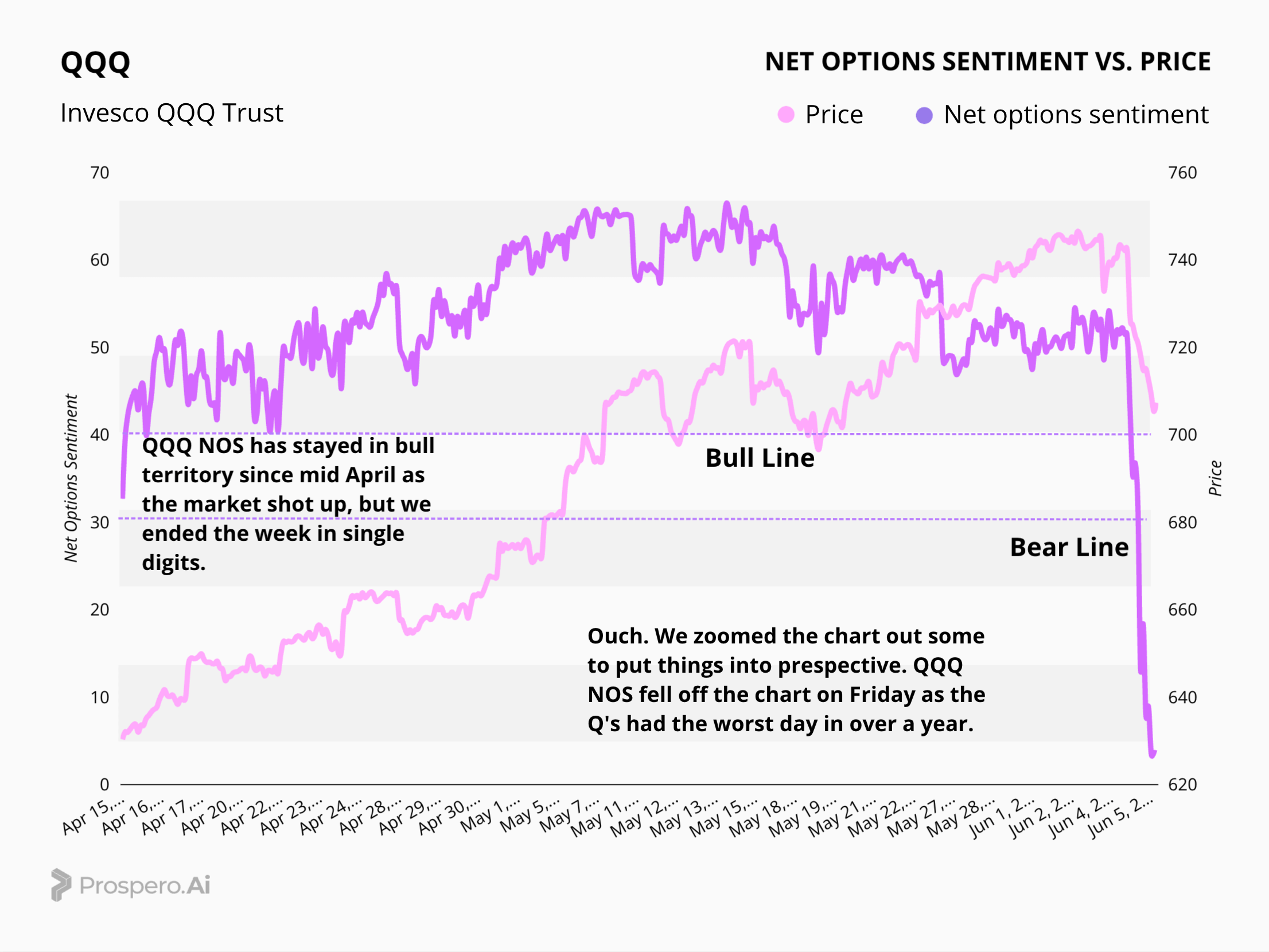

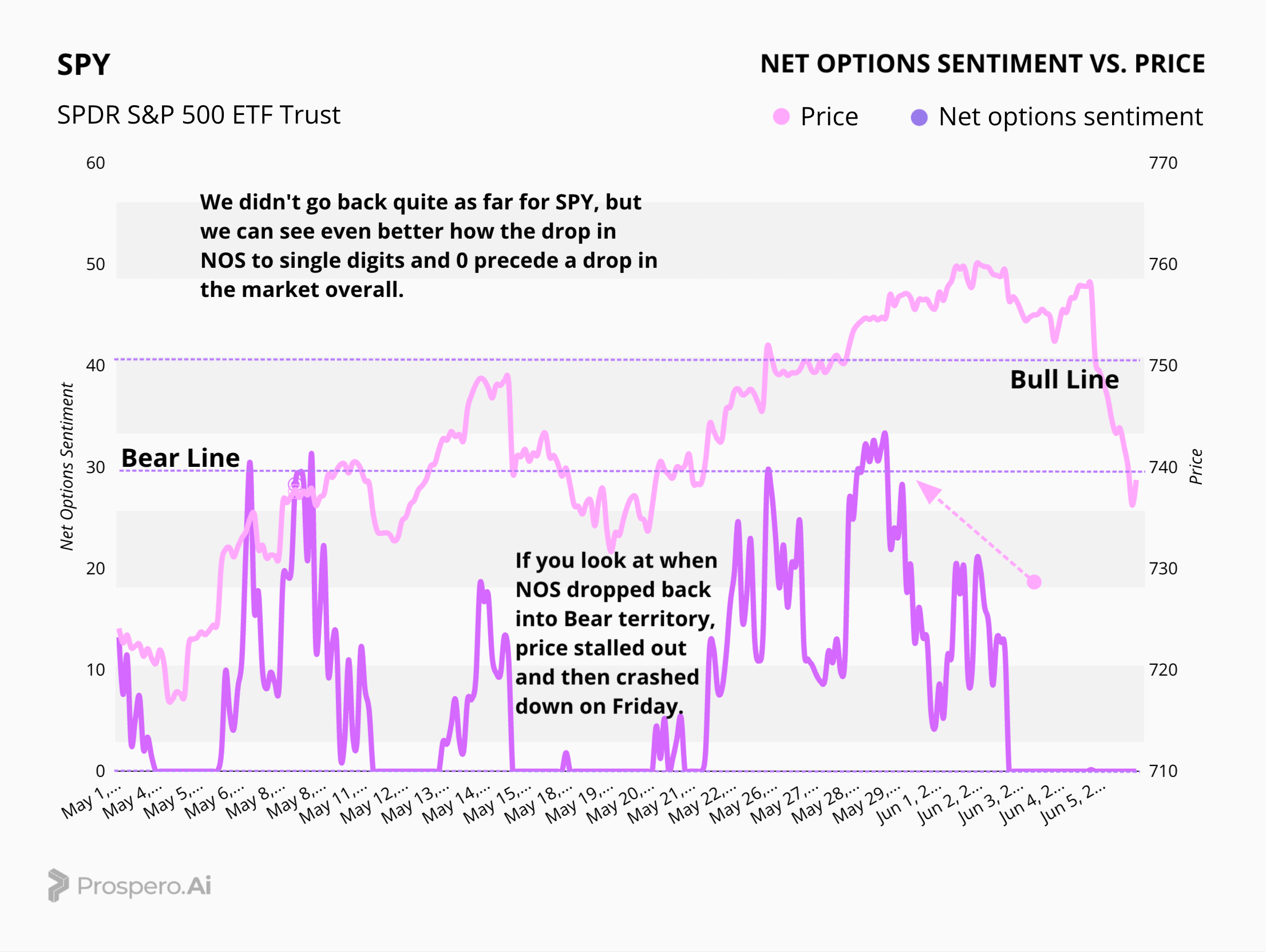

After a highly bullish run that saw QQQ Net Options Sentiment climb into the 60s, the week ended at 4. With SPY sitting at 0, we’re looking at a concerned market again. An unsettled Iran situation, an underwhelming GDP print, soft consumer sentiment, and worrying inflation reads have not slowed down this freight train of a market. But what goes up must come down, and we think one particular event might be elevating the caution.

FOMC, June 17th. Rates staying steady is a 98% foregone conclusion, so this isn’t about the decision. It’s about the tone of Kevin Warsh’s first meeting and how the votes play out. He was put in the chair to cut. The data since he was sworn in, a 172K jobs print against 85K expected and CPI running 3.8% and climbing, says the opposite. That tension is the whole trade. I asked for some probability analysis from Claude to help play out the game theory going into this meeting.

Scenario A: The Hawkish Hold (~65–70%)

This is the base case, and it’s the dull one, which is exactly why it’s the most likely. The committee holds, the language pushes the cut timeline out into late 2026 or 2027, and Warsh keeps the door technically open without shutting it either way. Eleven of the twelve members wanted no cut last time and several leaned toward a hike, so Warsh can’t do anything dramatic on his debut even if he wanted to. The market has mostly absorbed this already, so the reaction is small: I’d put SPY in a -0.5% to +0.5% chop and QQQ in a -1.5% to +0.5% band, with the downside skew on QQQ if the cut timeline visibly slips. Nothing breaks. The rotation book keeps grinding because higher-for-longer is the thesis. You don’t need fireworks, you need the easing clock to keep getting pushed back, and it already is.

Scenario B: The Dovish Tilt (~20–22%)

This is the squeeze scenario, and the wrinkle that sets it apart from a normal dovish surprise is that the dovishness most likely comes from Warsh’s mouth, not the committee’s hand. Picture him leaning into a softer tone in the presser to keep the White House off his back, even while the dot plot and the dissents read hawkish underneath. If the June CPI prints cool the day before, this gets real, and the most beaten-down, most rate-sensitive names run hardest. SPY climbs +1% to +2%, QQQ leads at +2% to +4%, and the SPY/QQQ leadership flips for the first time in weeks. This is the one to respect if you’re short tech. A dovish-sounding Warsh is what wakes up the dip-buyers in semis and software and puts the squeeze on names like ADSK and TRMB. Watch the CPI print, it’s the trigger.

Scenario C: The Hawkish Break (~8–12%)

The tail, and it’s a thinner tail than it would have been under Powell. For this you need a real hawkish escalation: hikes named as a live option, dots moving up, the “no cuts in 2026” story stamped in ink. The economics support it. The politics don’t. A chair installed to ease is the last person who wants to lead his first meeting waving a hike, so I’ve cut this down. But if it fires, it’s the cleanest payday for the rotation. SPY takes -1.5% to -3%, QQQ takes roughly double at -3% to -5%, and the Nasdaq hunts for lower levels as long-duration growth gets repriced fast. This is the one where every short in the book works at once.

Where I land

Blend it and the weighted move is small, SPY around -0.2% and QQQ around -0.5%, but don’t let the average fool you. The expected move is tiny because the fat middle is a near-priced hold. The money is in which tail fires, and the variance is wide. The bigger point: Warsh can’t escalate at his debut, so September, not June, is the more probable venue for any real hawkish action. June is a tone-and-dot-plot event. Trade the language, not the decision, and the CPI print the day before is what tips which way the language goes.

The irony nobody’s pricing: Trump’s guy can’t deliver Trump’s cuts

Here’s the part that makes this debut genuinely strange. Warsh was Trump’s pick precisely because the White House wanted rate cuts. Trump spent two years going after Powell over this exact issue, and Warsh arrived having publicly called for “regime change” at the Fed. The expectation was simple: install the guy who’ll ease. But the chair doesn’t set rates by decree. He gets one vote out of twelve, and he walked into this committee replacing Stephan Miran’s seat, which means the only member who wanted a cut at the last meeting is the seat Warsh now holds. The other eleven wanted to hold, and several leaned toward hiking. That’s not a committee you flip with a gavel and good intentions.

So Warsh inherits a vise. The data since he was sworn in, hot jobs, CPI at a three-year high and rising, energy pressure feeding through, has made the case for cuts weaker, not stronger, at the exact moment he’s supposed to deliver them. He’s left with two bad options: vote to hold, with members openly pushing for a hike, and take Trump’s public wrath, or cast a lonely minority vote for a cut he can’t win, which would make him the first Fed chair in modern history to be outvoted on his own committee on monetary policy. Neither is a position of strength. And we got a live preview of the pressure this weekend, when Trump went on Meet the Press to say it would be “wrong” for the Fed to raise rates, pushing back against the very market sentiment the jobs report created.

That’s why I’m fading the hawkish tail in June and pointing at September. Not because the economics don’t justify a hawkish stance, they increasingly do, but because Warsh has every personal and political reason to avoid validating a hike on day one, even as the committee under him drifts that way. The most likely outcome is the awkward middle: a hold the data demands, wrapped in language soft enough to keep the White House from blowing up, with a dot plot that quietly tells a more hawkish story than the chair’s tone does. Watch for that gap between what Warsh says and what the dots show. That divergence is the new signal this cycle, and it didn’t exist under Powell.

So what are we watching for?

To me, the game theory says it all. For the first time I can remember, the setup nets out negative going into the FOMC, even with a hand-picked, more dovish chair in the seat. This is what we always warn against. When there’s a negative event on the horizon, even a short-term one, you sometimes get a rush to sell before everyone else sells as the event approaches. It’s probably as much about the fear of a hot CPI print as the meeting itself, but it all wraps into one.

At Prospero we’re always trying to fit the story to the data, and the move out of Growth and into Value has been clear. Go back even a month and Large Cap Value is the best-performing group. We’re starting the week net short for the first time in a long time, but make sure to watch our Cap / Value chart at the open. If it’s another value day, I’d seriously consider leaning further into it.

A WORD FROM ME

Well like everyone Friday definitely hurt, but we were positioned almost neutral so were spared the full force of the drop. We are still doing great, currently 39% above the market on an annualized basis, with a 57% win rate against SPY benchmarks.

Our short intro + learning videos get you up to speed on how best use our letters and app to increase your wins.

Monday’s stream 6/7 is at the normal time 11AM. But we are doing a special marathon stream on Friday afternoon 6/12 1:30PM-3PM ET so I can make sure to get all your questions before my break!

Track all of your investments in real time with our app. Prospero’s proprietary AI tech updates key options signals like Net Options Sentiment, Upside and Downside every 3 minutes.

WARSH YOUR STEP?

Market/Macro Update w/ Cap/ Value Analysis

QQQ and SPY Net Options Sentiment

Sector Analysis

How we view the Sector performance and momentum

Portfolio Strategy

Putting it all together to make a portfolio that first controls for risks but also has upside

Longs

Adds —> Keeps —> Drops

Shorts

Adds —> Keeps —> Drops

Portfolio Summary

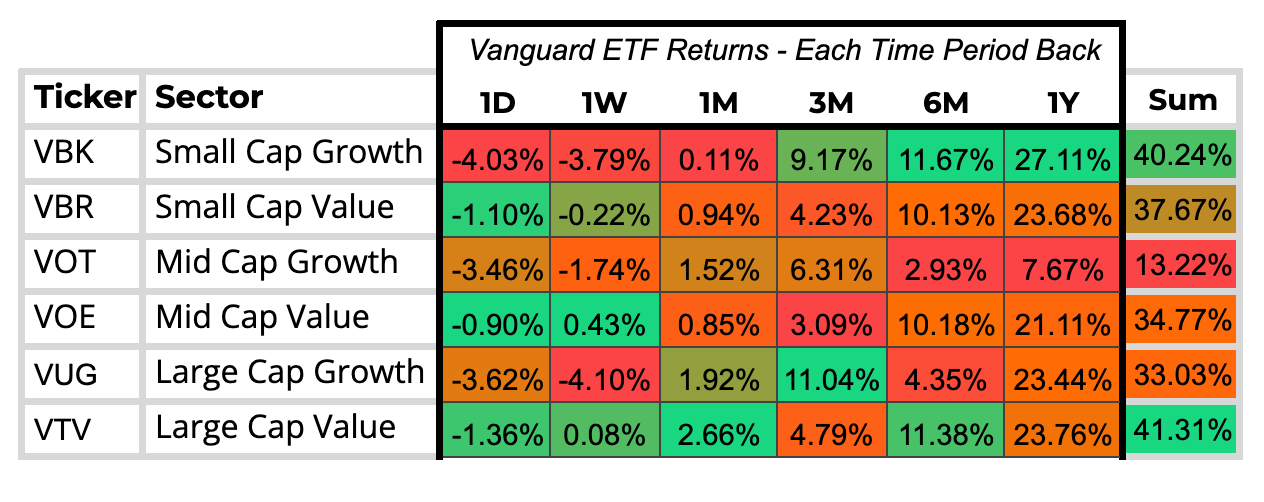

CAP / VALUE ANALYSIS

We are seeing a brutal short-term rotation out of Growth. Looking at the daily and weekly windows, Growth sectors took a severe beating across the board. Small Cap Growth and Large Cap Growth were the hardest hit, plunging roughly 4% over the last week. Mid Cap Growth wasn’t spared either, dropping over 3.4% in just a single session.

On the flip side, Value acted as a crucial defensive anchor amidst the heavy selling. While Growth bled out, Mid Cap and Large Cap Value remained completely resilient, essentially flatlining to slightly green on the week. The main takeaway right now is clear: capital is aggressively fleeing the higher-beta growth names and taking shelter in the stability of Value.

Ouch. We had to zoom the chart out to put things into perspective, and the shift is drastic. After staying comfortably in bull territory since mid-April and supporting the market's steady climb, QQQ Net Options Sentiment completely fell off a cliff on Friday. This happened early signaling a much worse day was on the way. It is why we sent out an early Bear alert. The Q's just suffered their worst day in over a year, and NOS reacted violently, plummeting all the way down into the single digits to end the week. This is a massive, immediate breakdown in bullish sentiment that completely changes the near-term landscape, and we will be monitoring this very closely to see if it acts as a leading indicator for further downside.

The predictive power of Net Options Sentiment is on full display here. If you look closely at the chart, the sharp drops in NOS—plummeting into single digits and hitting the zero line—consistently act as a leading indicator, preceding drops in the broader market. We saw this play out perfectly late in the week: as soon as NOS collapsed back into Bear territory, the price action stalled out and ultimately crashed down on Friday. This is exactly why we track this data so closely. These aggressive divergences in sentiment provide a clear, objective signal and the perfect window of opportunity to hedge your portfolio or sell off exposure before the bottom falls out.

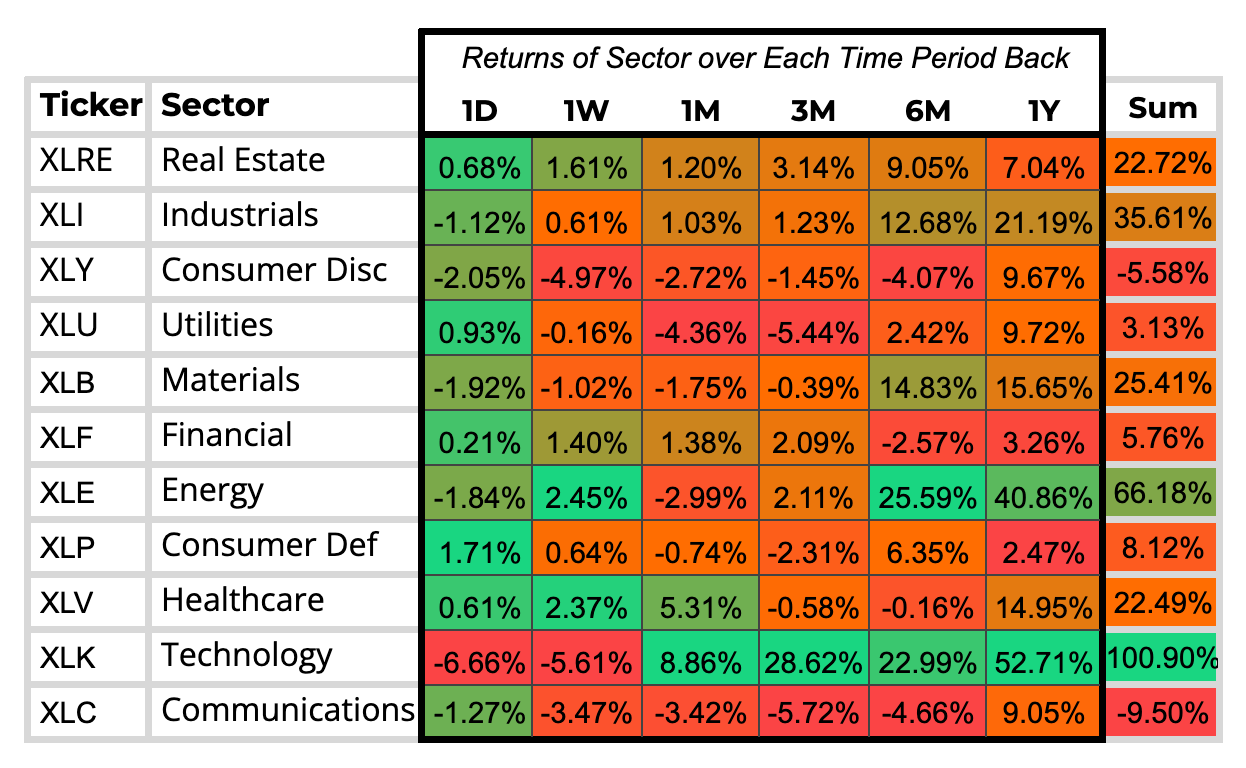

SECTOR ANALYSIS

We are witnessing a violent shift in market leadership. Technology absolutely cratered, suffering a massive 6.6% drop in just a single day and dragging its weekly performance down to a brutal 5.6% loss. Consumer Discretionary was caught in the exact same downdraft, bleeding roughly 5% over the week, while Communications also took a heavy 3.4% weekly hit.

Capital is aggressively fleeing these former high-flyers and looking for cover. While the broader tech and discretionary markets bled out, Healthcare and Energy emerged as the primary safe havens, posting strong weekly gains of 2.4% and 2.5%, respectively. The data is screaming that the momentum trade in tech has violently snapped, and institutional money is rapidly rotating out of high-beta tech and into defensive and commodity-based resilience. The question is, will the trend continue or will this sharp reversal lead to better valuations that get bought up.

PORTFOLIO STRATEGY

QQQ Net Options Sentiment dropped off a cliff to end the week at 4, and SPY has been pinned at 0. One bad day does not equal a trend, but we are starting the week much more cautious until the data tells us otherwise. Starting the week bearish with 5 shorts and 3 longs.

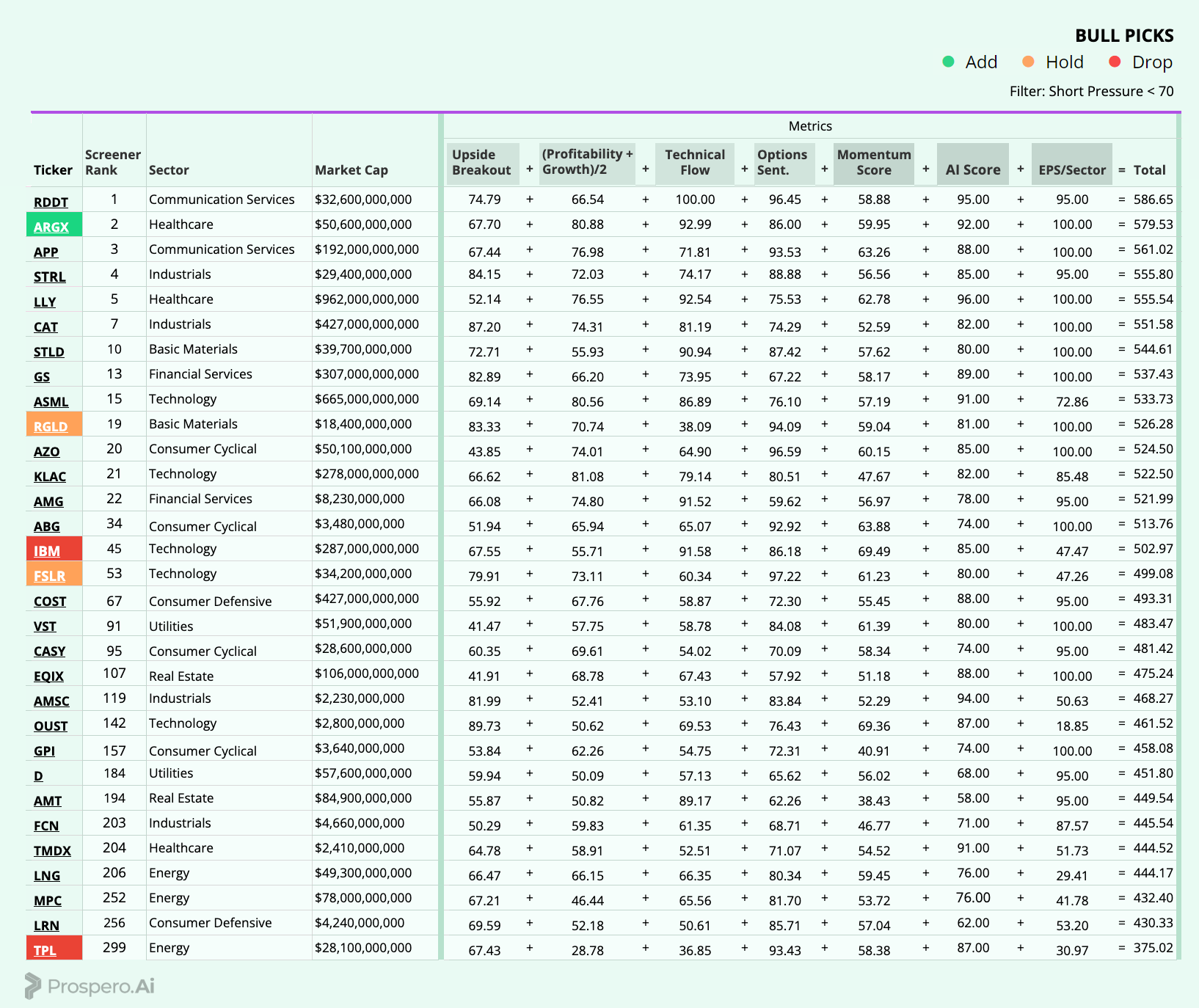

Long / Bull Moves – ARGX Add / FSLR, RGLD Holds / IBM, TPL Drops

Adds

ARGX was added for its great scores overall and to get into Healthcare, which was a top sector last week.

Holds

RGLD was held for its strong Upside and Net Ops and FSLR was held for its high Net Ops.

Drops

TPL was dropped as it ranked poorly in our screener overall and IBM was dropped for its dropping Net Ops and to pair down our Tech exposure.

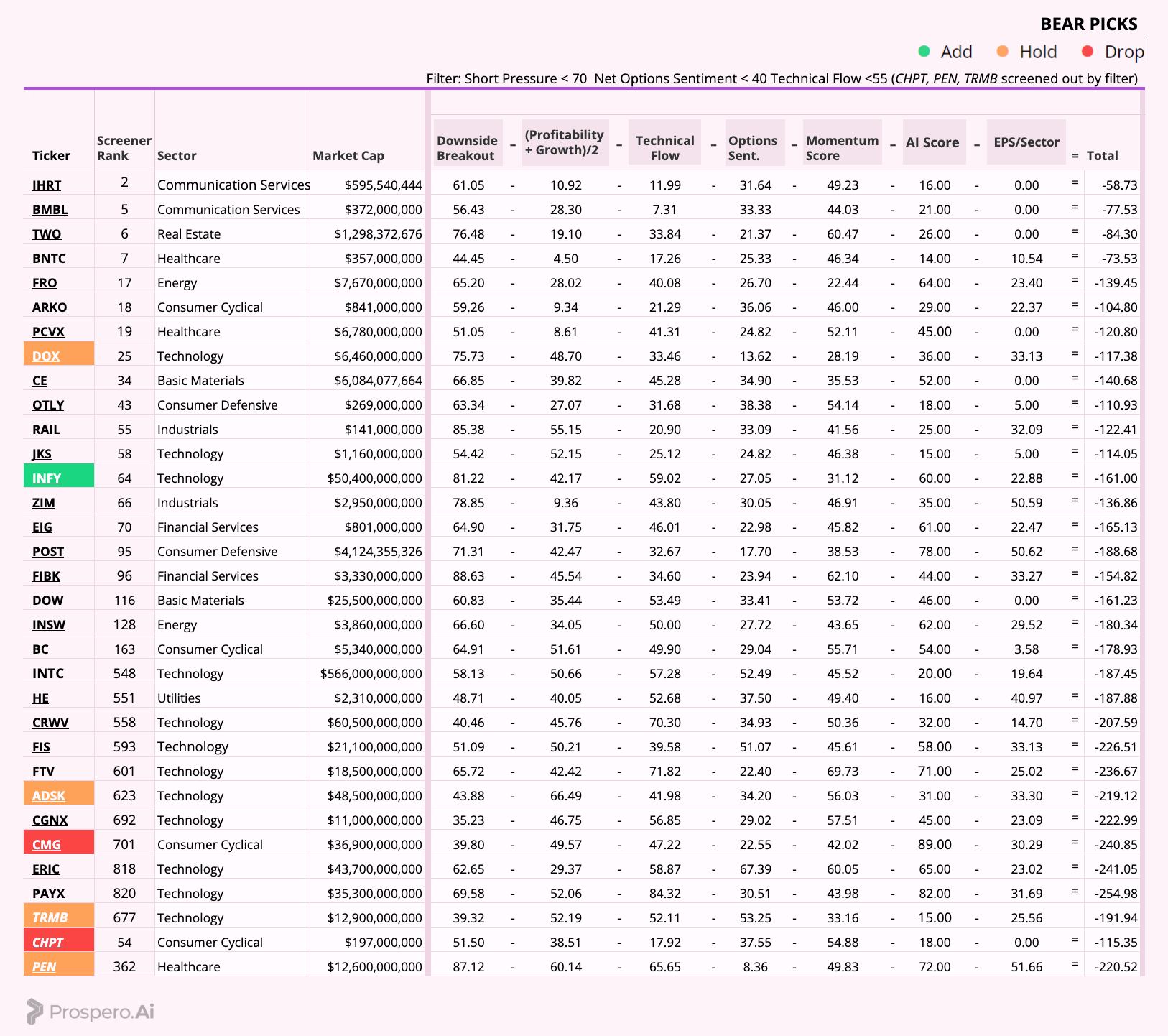

Short / Bear Moves – INFY Add / ADSK, TRMB, PEN, DOX Hold / CMG, CHPT Drops

Adds

INFY was added for its high downside and poor Net Ops.

Holds

DOX was held for its high ranking in our screener overall, ADSK was kept for its poor Net Ops, TRMB was held for its poor AI score, and PEN was kept for its high Downside.

Drops

CHPT was dropped as it was screened out and CMG was dropped for its high AI score and increasing Momentum score.

Portfolio Summary

Long / Bull Moves – ARGX Add / RGLD, FSLR as holds / IBM, TPL drops

Short / Bear Moves – INFY Add / TRMB, ADSK, PEN, DOX holds / CHPT, CMG as drops

3 Longs: ARGX, RGLD, FSLR

5 Shorts: INFY, TRMB, ADSK, PEN, DOX